| eRate Newsletter |

July 18, 2016 |

|

| |

IRS Discount Rate: August 1.4%

The valuation rate for gifts to new pooled income funds

is 1.2% in 2016 . |

|

|

Tracking Gift Annuity Market Values: Unitization v. Fund Accounting

There are two general approaches to tracking gift annuity market values: Fund Accounting and Unitization.Tracking gift annuity market values allows the charity to monitor the health of its gift annuity program on a gift-by-gift basis, as well as on a pool-wide basis.

This tracking allows a charity to identify individual problem annuities and, once identified, to consider the possibilities for ameliorating their negative effect on the performance of the gift annuity program overall.

|

|

| |

|

|

| |

IN THIS ISSUE |

|

| |

|

| |

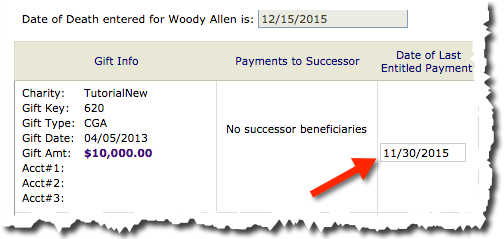

Quick Tip: Record Death in GiftWrap

Recording the death of a CGA beneficiary in GiftWrap is a fairly straightforward process. However, there are some details to be on the lookout for. One such detail is the instance in which one or more payments after the date of death will not be returned to the charity. Under these circumstances, the “Date of Last Entitled Payment” must be adjusted. Here is an example:

- The beneficiary passed away on December 15, 2015.

- A payment was sent to the beneficiary on December 31, 2015 and was cashed.

- The charity was notified of the beneficiary’s death after the December 31st payment was cashed.

- The charity is not expecting to receive reimbursement for the December 31st payment.

When recording the death, GiftWrap will default the “Date of Last Entitled Payment” to the most recent payment date prior to the date of death. In this case, and given a monthly payment schedule, the default date would be November 30th. Since you do not expect reimbursement for the December 31st payment, you will want to edit the “Date of Last Entitled Payment” so that it reflects December 31st, and not the default date of November 30th.

|

|

| |

Marketing Corner: The Simplest Way to Improve Conversions

Non-profits can learn a lot from the for-profit marketing world. The end goal of non-profit marketing is still the conversion, just like someone selling a product. Improving conversions leads to more donations. Find out how to improve your conversions and talk to more donors today.

Read More>>

|

| |

Make Your Next Gift Annuity Mailing More Effective with BatchCalcs

Fall is the most popular time of the year to mail to gift annuity prospects. Every year at this time, we help scores of clients add impact to their gift annuity mailings by personalizing the benefits quoted for each recipient. With BatchCalcs, you can tell each prospect the annuity amount, charitable deduction, and tax-free portion they will receive for a gift annuity of a specified amount. Whether asking your current gift annuity donors for a repeat gift or encouraging prospects to fund their first gift annuity, BatchCalcs will help you raise more gifts.

Learn More>>

|

| |

Projecting Future Income from Bequest Expectancies

Bequests are the largest source of income for most charities with planned giving programs. A simple analysis of your bequest expectancies can translate donors' commitments into projected future income streams. Learn how to project these valuable gifts.

Read More>>

|

| |

Planned Giving for Canadians Updated for 2016

On July 8, we released the latest update of Planned Giving for Canadians. This comprehensive guide is an essential resource for development officers at U.S. and Canadian charities who wish to offer their Canadian donors a full range of effective giving options. The 2016 update provides new material on endowments, further explains the new rules affecting credits for bequests and other end-of-life gifts, describes changes in the tax credit in Quebec, and much more.

Learn More>>

|

| |

When PGM Sells Assets in Its Illustrations

Planned Giving Manager gives our clients the ability to estimate how a planned gift will perform based on specific investment assumptions. These investment assumptions can include selling all plan assets in a particular year or selling a specified percentage of the plan’s assets each year. In both of these cases, PGM assumes that a sale occurs on the first day of the year. For example, if you vary investment assumptions and indicate a sale will occur in 2020, then PGM will assume the sale is on 1/1/2020. This timing will affect how much capital gain is realized as a result of the sale, since appreciation that occurs during 2020 will not be included.

The one exception to PGM selling assets at the beginning of the year is when a gift plan must sell assets in order to meet its payment obligation at the end of the year. In this case, the sale occurs on the last day of the year. For example, if a standard charitable remainder unitrust (CRUT) must distribute $5,000 at the end of the year, but earns only $3,000 of net income, PGM will assume a sale of $2,000 of the CRUT’s assets on the last day of the year in order to make up the difference. Again, this timing will affect how much capital gain is realized as a result of the sale, since appreciation that occurred during the year of sale will be included.

|

| |

Transforming Life Income Gifts into Current Gifts

By their nature, life income gifts are deferred gifts. The charity's use of the funds is delayed until a future date, normally the death of the donor. In this case, the donor usually does not see the gift in action. Transforming life income gifts into another gift vehicle can be mutually beneficial.

Learn More>>

|

|

|