|

|

|

|

|

|

|

|

|

“Please, Sir, I Want Some More”

The Plight of Orphan DAFs

What happens when there is money left in a donor-advised fund after the last donor-advisor has died? Where does that money go? Who decides how the money is used? Like a street urchin in a Charles Dickens novel, an “orphan donor-advised fund” can sometimes achieve great expectations or, sadly, pass invisibly without much impact. And, like Dickens’ obsession with orphans, there are those who are concerned about the increasing orphan population and some who would exploit these orphans for their own purposes.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

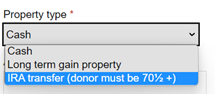

colleagues and me. With the recent legislative change and new gift opportunity to fund life income gifts with IRA assets, we wanted to ensure that our colleagues felt comfortable preparing proposals within PGM Anywhere. It is always nice to have a refresher of the features in PGM Anywhere as well. We reached out to the Client Services team for a custom training. They were very helpful in coordinating the session and providing an effective training for system colleagues and me. During the training, not only did Kara show us the workaround in the system but she also shared an overview of the new legislative change, requirements, the updated narratives, etc. My colleagues and I thought it was a very insightful training for the new gift opportunity they are marketing and a reminder of the services we have available through PG Calc. Kara also reminded the group about the support services PG Calc offers. Thank you again for your support and an informative session!”

colleagues and me. With the recent legislative change and new gift opportunity to fund life income gifts with IRA assets, we wanted to ensure that our colleagues felt comfortable preparing proposals within PGM Anywhere. It is always nice to have a refresher of the features in PGM Anywhere as well. We reached out to the Client Services team for a custom training. They were very helpful in coordinating the session and providing an effective training for system colleagues and me. During the training, not only did Kara show us the workaround in the system but she also shared an overview of the new legislative change, requirements, the updated narratives, etc. My colleagues and I thought it was a very insightful training for the new gift opportunity they are marketing and a reminder of the services we have available through PG Calc. Kara also reminded the group about the support services PG Calc offers. Thank you again for your support and an informative session!”